Why money keeps choosing Montenegro — and what still makes it hesitate

Montenegro does not compete on scale. It competes on density — of coastline, access, proximity and, increasingly, of capital that knows exactly what it is buying.

The country’s investment story is often reduced to real estate statistics and postcard imagery. But that framing misses the real dynamic. Capital does not arrive in Montenegro because it is picturesque. It arrives because the risk is legible. For investors placing long-term money, clarity often matters more than size. Montenegro has gradually learned how to make itself readable.

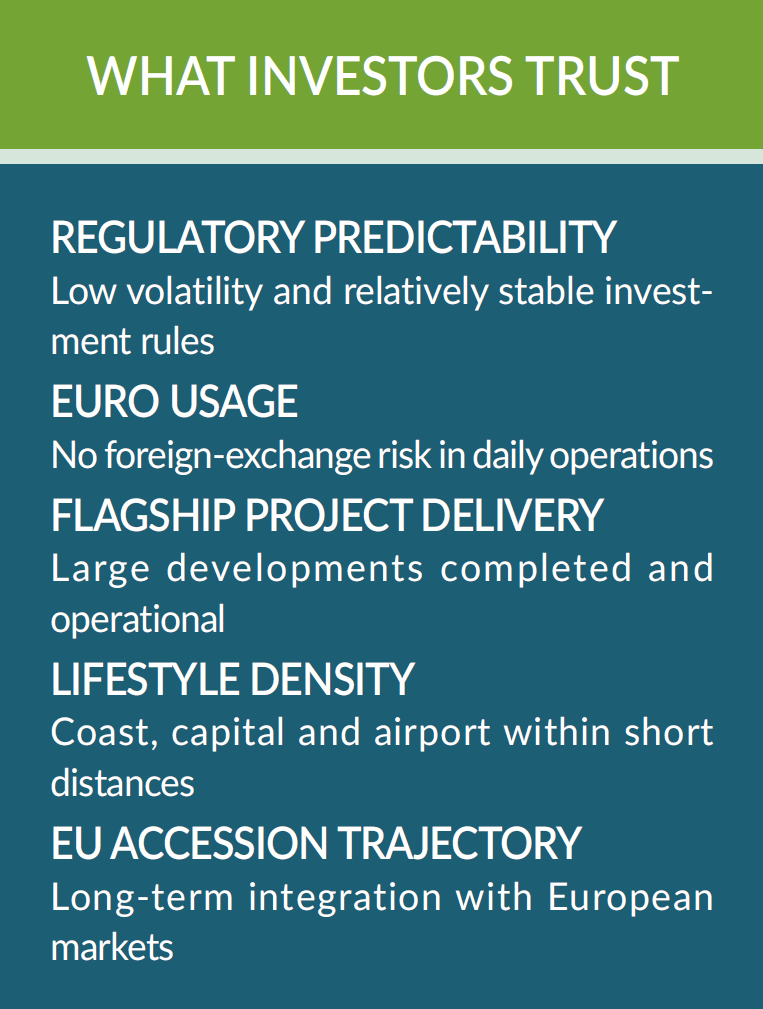

Foreign direct investment has remained resilient for more than a decade, with property continuing to absorb a large share of capital inflows. That pattern is neither accidental nor temporary. Real estate is typically where international capital tests a new market first — where resale value, jurisdictional risk and demand can be assessed quickly. Montenegro has passed that test repeatedly. What followed was confidence.

That confidence has visible landmarks. Porto Montenegro in Tivat, backed by international investors including the Investment Corporation of Dubai, was among the first developments to demonstrate that global standards could not only be introduced, but sustained. It was never simply a marina. It was designed as an ecosystem — residential, commercial and service-based — capable of keeping capital circulating rather than departing with the tourist season.

Further along the coast, the pattern repeats in different forms. Luštica Bay, developed by Orascom Development, was conceived less as a resort and more as a town — a bet on permanence in a country historically associated with seasonality. Portonovi in Kumbor introduced another scale of investment, combining hospitality, residences and marina infrastructure.

These projects serve a role beyond tourism. They function as signals. When they perform, other investors stop asking whether Montenegro works and start asking where they might enter.

Policy has reinforced that signal. Montenegro combines relatively low headline tax rates with the stability of euro usage, despite not being part of the eurozone. Coupled with a political narrative oriented toward European Union accession, this has created a rare regional proposition: predictability without the complexity of larger markets.

Montenegro does not advertise regulatory stability loudly. Instead, it demonstrates it through repetition. Investors return because the rules tend not to change mid-sentence.

Capital Check: Montenegro

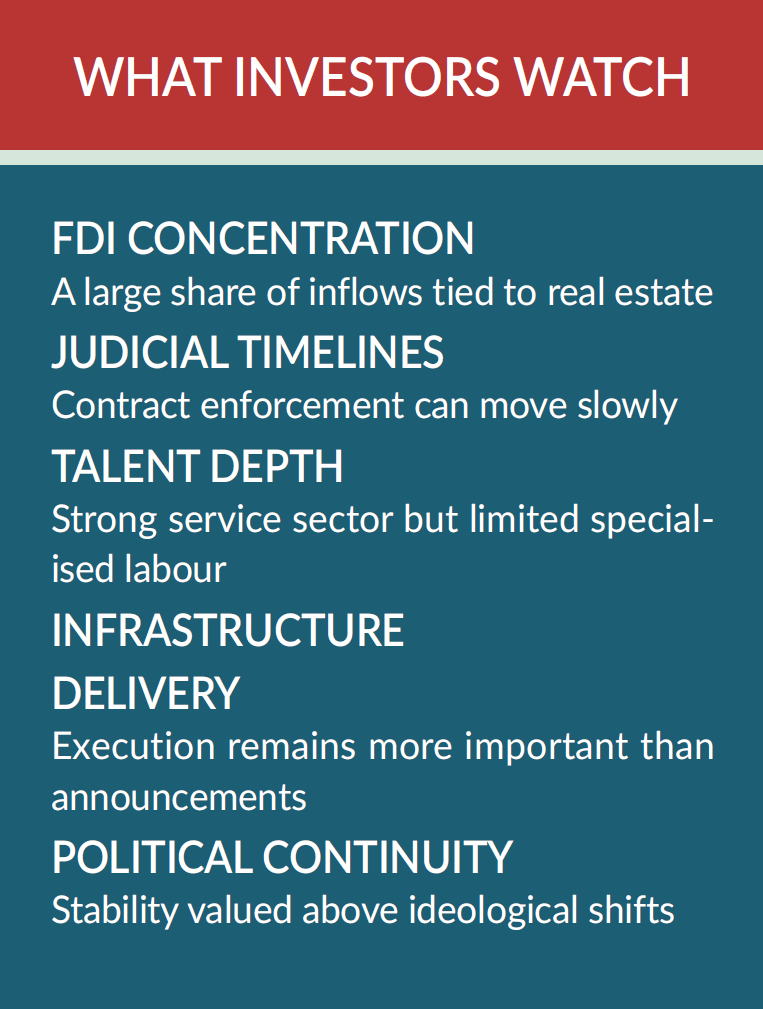

Yet confidence, once established, becomes demanding. Montenegro’s foreign investment structure remains heavily concentrated in property and tourism-linked assets. Productive investment — in advanced services, export-oriented sectors and parts of the energy economy beyond renewables — has grown more slowly than policymakers would like.

The question is no longer whether Montenegro is attractive to investors. That debate has largely been settled. The more relevant question is whether the investment base can broaden.

Capital notices when ambition outruns execution. It also notices when comfort replaces reform. Montenegro is not there yet — but it is closer than it sometimes admits.

That tension defines the next phase of the country’s development. Montenegro’s greatest advantage has always been speed: a small system where decisions travel quickly and proximity compresses distance between capital and lifestyle.

Its risk lies in mistaking desirability for inevitability. Capital stays where it can grow, not just where it can rest.

The country has already answered the hardest question — whether global investors trust it. They do.

The remaining test is quieter, and more consequential: whether Montenegro can turn confidence into diversification, and reputation into resilience.

Money is patient. But it is not sentimental. And it is already watching what comes next.

Where capital is physically reshaping Montenegro — see the Investment Map on page 38.