Governor Irena Radović on banking resilience, SEPA integration and the structural realities of operating without monetary autonomy.

Montenegro’s financial system rarely makes headlines — and that is precisely the point. In a small, euroised economy without independent monetary policy, stability is not accidental; it is constructed through supervision, discipline, and institutional design. As Montenegro positions itself as a serious investment destination, the health of its banking sector becomes more than a technical matter. It becomes a signal. Dr Irena Radović, Governor of the Central Bank of Montenegro speaks in Montenegro Means Business about resilience, credit dynamics, SEPA integration and the structural trade-offs of euroisation — and what financial stability means for businesses operating in and with Montenegro.

How would you assess the current state and resilience of Montenegro’s banking sector?

Montenegro’s banking sector is stable, liquid, and strongly capitalised, reflecting a sustained reform agenda led by the Central Bank to align the regulatory and supervisory framework with European Union standards.

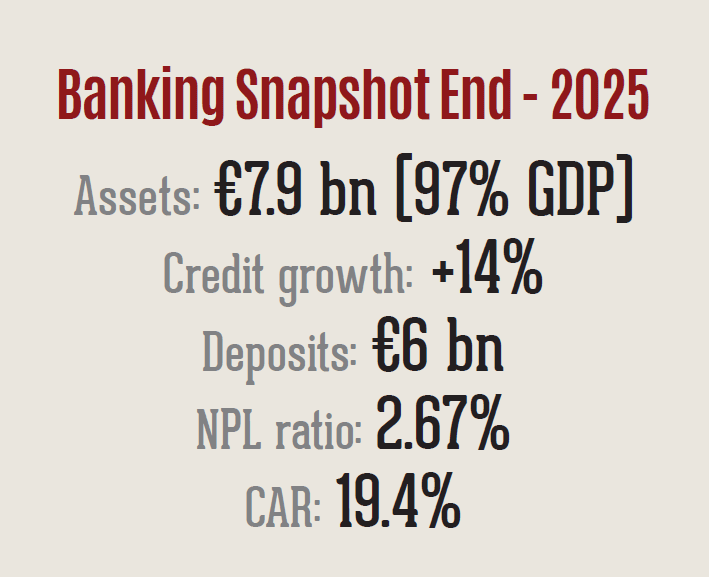

At the end of 2025, total bank assets reached EUR 7.9 billion (over 97% of GDP), with annual growth of around 9%, confirming the sector’s central role in financing the domestic economy. Credit activity remains robust, with year-on-year growth exceeding 14%, while deposits of nearly EUR 6 billion (around 75% of GDP) indicate sustained public confidence.

Asset quality continues to improve, with non-performing loans at a historical low of 2.67%, confirming that credit expansion is grounded in prudent underwriting and effective supervision. A capital adequacy ratio of 19.4%, well above regulatory requirements, further underscores resilience.

Euroisation provides stability and credibility, but requires disciplined institutional policy

Progress has also been made in meeting the closing benchmarks for EU negotiation Chapters 4 (Free Movement of Capital), 9 (Financial Services), and 32 (Financial Control), demonstrating alignment with the EU acquis.

A key milestone was Montenegro’s accession to SEPA in November 2024, enabling integration into the European payments market under EU rules.

In parallel, the Central Bank is advancing the TIPS Clone project to strengthen instant payment capabilities and interoperability with European infrastructures.

Strong fundamentals, regulatory convergence, and integration into European financial infrastructures position Montenegro’s banking sector as resilient and prepared for sustainable growth.

Is credit activity sufficiently aligned with the needs of the economy and investment projects?

From the supply side, there are no material constraints on financing sustainable, high-quality projects, reflecting ample liquidity and a sound banking system. Credit dynamics, however, are equally shaped by demand-side factors, including the bankability of investment proposals, financial discipline, and the long-term viability of business models.

Credit expansion can reach its full potential only within a broader reform framework that strengthens the business environment and institutional capacity. Within the constraints of a euroised system, the Central Bank remains focused on preserving financial stability and enhancing financial infrastructure to support the real economy.

Credit growth depends not only on interest rates, but on the overall efficiency of the financial system and the cost structure of doing business. In this respect, Montenegro’s integration into SEPA represents a measurable structural improvement.

According to preliminary World Bank indicators, average B2B transaction fees between Montenegro and SEPA countries have fallen from around 1% to approximately 0.04% of transaction value — a significant and immediate reduction in costs.

This efficiency gain frees resources for investment, expansion, and job creation.

Looking ahead, the Central Bank will continue alignment with European regulatory standards, including DORA and MiCA, while developing instant payments through the TIPS Clone system and maintaining a secure, predictable financial environment.

The objective remains clear: a resilient banking system that enables faster, more affordable financing aligned with productive investment needs.

In a euroised economy, where does Montenegro’s financial system gain strength, and where does it face constraints?

Euroisation provides tangible strengths, most notably monetary stability, low currency risk, and high credibility for investors and depositors. The use of the euro eliminates exchange rate volatility and anchors expectations — particularly valuable for a small, open economy. It facilitates cross-border transactions and supports financial integration with the European Union.

At the same time, euroisation entails structural constraints, primarily the absence of independent monetary policy instruments, including exchange rate flexibility and autonomous liquidity provision.

As a result, resilience relies more heavily on strong supervision, prudent risk management, and adequate capital and liquidity buffers.

In a system without access to monetary financing or seigniorage income, ensuring the financial sustainability of the central bank becomes particularly important. This requires robust institutional design, diversified revenue sources, and continued alignment with European standards.

Euroisation provides stability and credibility, but demands disciplined, institution-driven policy. The Central Bank therefore remains focused on regulatory convergence and institutional strength, embedding Montenegro’s financial system within the European framework while supporting long-term growth.